Since the Great Recession of 2008, governments across the World, in particular the United States, have struggled to implement policies conducive to a full and speedy economic recovery. Some initiatives have worked better than others, which can lead many to wonder if government should have even intervened at all. In this paper, I’ll examine a few intervention successes, as well as failures and explain why I believe the most promising of all the post-2008 economic recovery initiatives is the passage of the JOBS Act in 2012.

During the Great Depression, the world’s economy stubbornly refused to move from its state of equilibrium at the bottom of a trough. Preeminent economist, John Maynard Keynes, recommended that the state increase spending to kick-start the economy. He theorized, like Thomas Malthus, that capitalism is prone to phases of scarce demand. However, where Malthus associated demand scarcity with under-consumption, Keynes believed that capitalists were to blame.

Capitalists are constantly speculating on future demand, evaluating what their competition is doing, trying to predict what they will do and making their most important decisions based on imperfect information. Keynes recognized that these capitalists, sensing any pessimistic indicator during their speculation, will be the first to “jump ship” and cut or cease their investments (Yanis Varoufakis, 2011, p. 205). Keynes argued that this isn’t irrational behavior, but instead, exactly what we would predict from capitalists in an indeterminate process that forces them to make their decisions based on strategic game play.

According to Keynes, this is exactly what prolonged and deepened the Great Depression. When capitalists tighten their belts they cut spending, stop hiring, hoard cash, lay off employees, etc. Capitalists’ reluctance to invest their money can trigger a recession, pull a recession into a depression and help keep a depressed economy in equilibrium. These decisions ripple through the economy as competitors and suppliers react to the permeating pessimism. Eventually, the retrenchment on Wall Street spreads to Main Street, affecting consumer spending and confidence in a negative feedback loop. Once settled into this negative stasis, it can be difficult, if not improbable, for the “invisible hand” to kick-start the economy again. Business owners lay off workers because they foresee retrenchment and decide to tighten their belt, consumers begin to cut household spending because they’ve been laid off or see their neighbors, family and/or friends laid off, capitalists then stop investing and cut production because of the drop in demand, ad infinitum to the point that a stalemate between consumers and producers occurs.

Keynes advocated for government spending during the Depression because without investment from capitalists or consumption by consumers, the government is the only single player left willing and able to make the first move to jumpstart the economy. However, Keynes didn’t offer any advice or recommendations on what type of government investments would be the most efficient use of tax payer dollars. He mused that “organized public works at home and abroad, maybe the right cure for a chronic tendency to a deficiency of effective demand” (Keynes, 1944). By the end of the 1930s, the chronically depressed economy was resuscitated only by the immense government spending required to conduct and facilitate the largest war humanity has ever witnessed. Clearly, in hindsight, this was not the government investment most economic advisers and policy makers would have had in mind.

In more recent times, the Troubled Asset Relief Program (TARP) “was created to restore the nation’s financial stability and restart economic growth” after the collapse in 2008 (U.S Department of Treasury, 2013). There was and still is much debate about TARP. However, the alternative to this government intervention in 2008 would have at least equated to hundreds of thousands of job losses with entire industries, like the automobile industry, on the brink of bankruptcy and/or possible dissolution (U.S Department of Treasury, 2013).

We will never know definitively whether or not government intervention in 2008 prevented the Great Recession from becoming a second Great Depression, but the most influential policy makers and advisers, former Federal Reserve Chairman Ben Bernanke among them, believed that without government intervention, “we would [have been] facing, potentially, another depression of the severity and length of the Depression in the 1930s” (Berry, 2010).

Yet, TARP only scratched the surface of the U.S Government’s intervention after 2008. Moving beyond a mere provider of safety nets, the “American Recovery and Reinvestment Act of 2009 — commonly referred to as the stimulus package” appropriated $840 billion with the goal of creating and saving jobs, as well as spurring economic activity and investing in long term-growth (Recovery Accountability and Transparency Board, 2013). The funds are being invested in areas such as education, transportation and infrastructure. The chart below shows the amount of cumulative funds awarded by category up until the end of the third quarter 2013:

Source: (Recovery Accountability and Transparency Board, 2013)

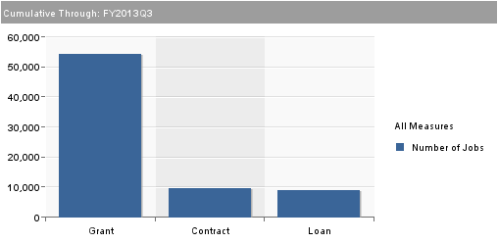

The total amount of recovery funds spent to date (3rd quarter, 2013) is approximately $275.67 billion. Through grants, contracts and loans, the government, through the Recovery Act, has created 72,242 jobs to date. That equates to approximately $3.82 million dollars spent per job created. The histogram below shows the number of cumulative jobs created up until the end of the third quarter, 2013:

Source: (Recovery Accountability and Transparency Board, 2013)

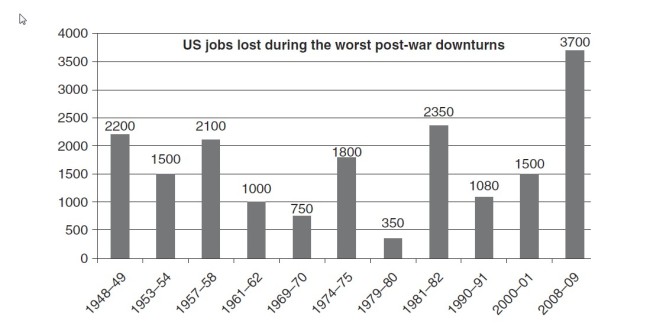

One need not be an economist to know that this ratio is anything but efficient in achieving the goal of job creation. On top of that, it’s a mere drop in the bucket compared to the approximately 3.7 million jobs that were lost in the economic downturn. The chart below shows the number of job losses in post-war downturns. The post-2008 downturn is the worst by far.

Source: (Yanis Varoufakis, 2011)

Looking a little closer at the Recovery Act, in March of 2009, the U.S Department of Energy, through the Recovery Act, gave Solyndra, a California based solar panel company, approximately $527 million in government backed loans. The company has since filed for bankruptcy, laying off more than 1,000 people in the process (Huffington Post, 2012). Certainly, this gives rise to questions about how long and how much the government should intervene during a time of crisis. Guaranteeing an early stage solar panel company isn’t the same as paying for roads and highways to be built. The government shouldered the majority of the risk associated with a start-up that had begun production only a couple of years prior to the government backed loan (Solyndra, 2013). The safety net that TARP provided might have been justified, but what about the parameters under which government acts as a capitalist would in normal economic times. Solyndra is indeed an example of the government’s failed role.

Through it all, the Federal Reserve has become the lender of last resort through the crisis and recovery (Bordo, et al., 2013). The low interest rates set by the fed have helped stimulate investment, but one of the biggest ongoing concerns is inflation. Already we are seeing interest rates creep back upward.

Perhaps many will agree that whenever possible, government should clear out of the way and let the market make more of the risky investment decisions. In 2012, the Jumpstart Our Business Start-ups (JOBS) Act, a bipartisan piece of legislation was passed with the intention of making it easier for small businesses, also our biggest job creators, to gain access to capital.

The JOBS Act allows small businesses to raise up to $1 million in a single year by offering up equity on an online portal and model similar to the popular crowdfunding site, Kickstarter (Colao, 2012). Before the passage of the JOBS Act, only accredited investors, (those individuals with income of $200,000 or more per year, joint income of $300,000 or more per year or a total combined net worth of $1 million or more) could invest in businesses without going through a broker (Investopedia, 2013). Now, under certain regulations designed to protect individual investors, anyone can invest a percentage of their income directly in early stage businesses directly through crowdfunding portals.

This piece of legislation is enabling the democratization of investing and seed capital for small businesses and will attract an estimated $200 trillion worth of investment capital being held on the sidelines worldwide (Barnett, SEC Finally Moves on Equity Crowdfunding, Phase 1, 2013). If this estimate is anywhere near accurate, my guess is that the JOBS Act will be the most effective long-term job creation initiative to spawn from the financial collapse of 2008.

One of the biggest sources of friction for a stalled economy is the lack of confidence in the market, the permeating pessimism that causes the negative feedback loop. Crowdfunding is revolutionary in that it not only democratizes investment, but also provides market validation by engaging a product or services’ early adopters.

Early adopters are the first buyers of new products and services. Crowdfunding allows innovators to prove their concept in the market by pre-selling to these early adopters and using those financial contributions as seed capital. Crowdfunding and Crowdfund Investing (CFI) are financial frontiers that hatched from the Great Recession of 2008. As investment dried up and banks refused to lend, crowdfunding provided an alternative.

In 2011, $1.47 billion was raised for projects through crowdfunding (Massolution, 2012). In 2012, that amount nearly doubled with approximately $2.7 billion raised and the forecast for 2013 is $5.1 billion (Massolution, 2013).

As this new financial innovation finds a foothold and matures, especially into the equity market, we could expect an estimated $300 billion in capital invested per year (Barnett, JOBS Act Title III: Investment Being Democratized, Moving Online, 2013).

Crowdfunding and CFI will not prevent recessions, but I wholeheartedly believe that this new investment vehicle will make our economy more robust in the long-term. It will help make the overall business cycle more robust as well, by providing access to capital for early stage ventures, allowing them to more quickly reach scale. If capitalists use crowdfunding as a mechanism for investment whenever possible, they will not have to speculate about the market; the proof of concept will be provided by successful crowdfunding campaigns. Successful crowdfunding campaigns will then signal to Angel investors and Venture Capitalists what is and is not worthy of larger investments.

Crowdfunding is quickly proving to be a game changer for small businesses. It is small businesses that create approximately 65% of net job creation (Dilger, 2013). Unfortunately, there isn’t really any data available that shows how many additional jobs are being created by small businesses because of access to crowdfunding capital. My prediction is that it will be substantial and at a much more efficient rate than job creation from the stimulus package. In fact, the establishment of the crowdfunding industry might prove to be the most positive offshoot to come out of the Great Recession of 2008.

Works Cited

Barnett, C. (2013, October 23). JOBS Act Title III: Investment Being Democratized, Moving Online. Forbes online. Retrieved December 1, 2013, from http://www.forbes.com/sites/chancebarnett/2013/10/23/sec-jobs-act-title-iii-investment-being-democratized-moving-online/

Barnett, C. (2013, July 19). SEC Finally Moves on Equity Crowdfunding, Phase 1. Forbes online. Retrieved November 30, 2013, from http://www.forbes.com/sites/chancebarnett/2013/07/19/sec-finally-moves-on-equity-crowdfunding-phase-1/

Berry, J. M. (2010). Skirting Depression. International Economy, 42-68. Retrieved November 30, 2013

Bordo, M. D., Ilzetzki, E., Ip, G., Mendoza, E. G., Mishkin, F. S., Reinhart, V. R., . . . Reinhart, V. R. (2013). No Way Out? : Government Intervention and the Financial Crisis. AEI Press. Retrieved December 1, 2013

Colao, J. (2012, March 21). Breaking Down the JOBS Act: Inside the Bill that Would Transform American Business. Forbes online.

Dilger, R. J. (2013). Small Business Administration and Job Creation. Congressional Research Service. Retrieved December 1, 2013, from http://www.fas.org/sgp/crs/misc/R41523.pdf

Glenn. (n.d.). Product Lifecycle: Do You Know Where Your Business Is? Washington D.C. Retrieved December 1, 2013, from http://www.beasuccessfulentrepreneur.com/product-lifecycle-do-you-know-where-your-business-is/

Huffington Post. (2012, July 30). Solyndra Bankruptcy: Solar Panel Company Won’t Pay Back Most of its $527 Million Government Loan.

Investopedia. (2013, December 1). Accredited Investor. Retrieved from Investopedia.com: http://www.investopedia.com/terms/a/accreditedinvestor.asp

Keynes, J. M. (1944). Collected Writings of John Maynard Keynes, vol. 27: Activities 1940-46: Shaping the Postwar World. Cambridge: Cambridge University Press.

Massolution. (2012). Crowdfunding Industry Report: Market Trends, Composition and Crowdfunding Platforms. Crowdsourcing.org.

Massolution. (2013). 2013CF The Crowdfunding Industry Report. Crowdsourcing.org.

Recovery Accountability and Transparency Board. (2013, November 30). Recovery Explorer. Retrieved from Recovery.gov: http://www.recovery.gov/Transparency/Pages/DataExplorerLanding.aspx

Recovery Accountability and Transparency Board. (2013, November 30). The Recovery Act. Retrieved from Recovery.gov: http://www.recovery.gov/About/Pages/The_Act.aspx

Solyndra. (2013, December 1). History. Retrieved from Solyndra.com: http://www.solyndra.com/about-us/timeline/

U.S Department of Treasury. (2013, November 13). About TARP. Retrieved from U.S Department of Treasury: http://www.treasury.gov/initiatives/financial-stability/about-tarp/Pages/default.aspx

U.S Department of Treasury. (2013, November 12). Auto Industry. Retrieved from U.S Department of Treasury Financial Stability: http://www.treasury.gov/initiatives/financial-stability/TARP-Programs/automotive-programs/Pages/default.aspx

Yanis Varoufakis, J. H. (2011). MODERN POLITICAL ECONOMICS: Making sense of the post-2008 world. Yanis Varoufakis, Joseph Halevi and Nicholas Theocarakis (2011). MODERN POLITICAL ECONOMICS:London and New York: Routledge.